Start 2024: The power battery market "got off to a good start" in March, the production of enterprises grew strongly

Date:2024-02-27 Views:512

From 2023 to 2024, through the difficult shadow of overcapacity, towards a new journey of one year, the opening performance of the power battery industry chain in 2024 is highly anticipated.

From the perspective of the market cycle law of the power battery and new energy vehicle market, from January to December, basically maintain a new linear growth trend, the market performance of the first quarter of the year determines the starting point of the annual growth of the power battery industry chain, but also the market confidence of the upstream and downstream of the power battery industry chain, as well as the expected outlook of annual shipments.

Based on the latest data, the market for new energy vehicles and power batteries in 2024 can be said to have ushered in a "good start."

According to the data released by the China Automobile Association, the sales volume of new energy vehicles in January 2024 reached 729,000, an increase of 78.8% over last year; In terms of power battery installed data, the installed capacity of power batteries in January 2024 was 32.3GWh, an increase of 100.2% year-on-year, which also had a good performance.

If the previous data is compared, the power battery industry chain in 2024 also implies a new round of growth potential.

Taking the data of January 2022 and January 2023 as an example, the sales volume of new energy vehicles increased by 141% year-on-year and decreased by 6% year-on-year respectively; In the power battery shipments, respectively, an increase of 86.9%, a decrease of 0.3%.

The different market performance of the power battery industry chain in the opening year of 2022 and 2023 also corresponds to the two distinct cycles of the rapid growth of the power battery industry chain and the downtrend of warehouse clearance. The good market performance in 2024 undoubtedly corresponds to the former.

The rapid reversal of production scheduling in the first quarter

From the perspective of the production scheduling of the lithium battery industry chain, a "V" type reversal structure is basically presented from December 2023 to March 2024.

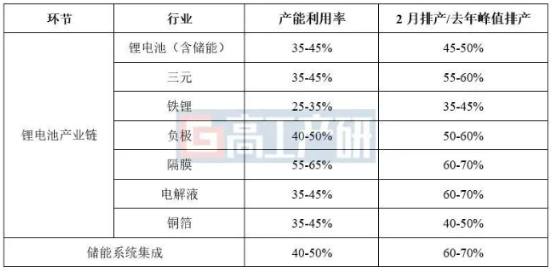

According to the high industrial research lithium battery Research Institute (GGII) data, from January to February 2024, the power battery production data generally declined, and it is expected that the capacity utilization rate of lithium batteries in February is 35-45%, the capacity utilization rate of terpolymer materials is 35-45%, and the capacity utilization rate of lithium iron materials is 25-35%, the relevant data are as follows:

On the one hand, the downturn in production data was affected by the impulse of the power battery industry chain at the end of December last year, and the enthusiasm of lithium battery enterprises to stock up in 2024 is not good; On the other hand, it is related to the traditional off-season of the first quarter of the power battery industry chain.

Affecting the opening of this year's production schedule is also based on the first quarter of 2023 production caused by excessive inventory clearance and price war, lithium battery companies in the first quarter of this year's production performance is obviously more cautious.

However, from the perspective of the production guidance of individual head battery companies in March, the recovery trend is very strong, and even the growth of 70-80% compared with February's production. This also means that the capacity utilization rate of some battery companies is expected to reach more than 70%.

Compared with the same period in 2023, the capacity utilization rate of lithium battery enterprises in the first quarter of the decline, as of April, the capacity utilization rate of some enterprises has fallen below 40%, until May or even June 2023, there is a warming up of production scheduling and orders. In terms of capacity utilization, even in the Ningde era, the capacity utilization rate rose to about 70% in the third quarter of 2023.

In contrast, in the beginning of 2024, lithium battery enterprises will recover more rapidly from the low capacity utilization rate, which is also expected to accelerate the trend of the downstream of the power battery industry chain from weak to strong in 2024.

Battery shipment or rewelcome high

Since last year, after the pace of expansion, inventory levels, procurement strategies and other comprehensive adjustments, the whole industrial chain of the lithium industry has gradually returned to a healthy level, especially the industry has reversed only focus on the "volume" level of capacity expansion, transformed to the quality and efficiency of battery products.

As an important guideline for annual shipments, the market performance of the power battery industry chain in the first quarter "underwrites" the lower limit of annual shipments.

A number of industry leaders said at the annual meeting that after the second half of 2024, from batteries to materials, the market will continue to usher in a cyclical inflection point.

In terms of price, the upper and middle reaches are conducive to the lower reaches, and the penetration rate of new energy vehicles is accelerated.

Market data show that in January 2024, the average price of power battery cells fell 4-7%, and in the case of further compression of materials and manufacturing costs by battery companies, the price of power battery cells is expected to further decline this year.

Recently, the new energy vehicle enterprises represented by BYD took the lead in the first shot of price reduction, and the starting price of Qin PLUS Glory edition and Destroyer 05 Glory edition was reduced to 79,800 yuan. Including Wuling, Changan, Nezha and other car companies have followed up, announcing price cuts for a number of models.

The price range of 5-150,000 yuan as the core market of domestic passenger cars, but also the highest proportion of fuel vehicles in the field, the BYD Qin PLUS as the representative of the plug-in tram price into 100,000 yuan, the new energy vehicle market boundary to further expand, the focus of the replacement of oil and electricity also from 100,000 to 200,000 yuan range down to 100,000 yuan.

With the arrival of the market inflection point of the power battery industry chain and the promotion of the market strategy of price for volume, power battery shipments are expected to usher in a new high in 2024.

According to the data of the high-tech lithium battery Research Institute, in 2024, China's lithium battery shipments are expected to reach 1089GWh, an increase of 23%, and China's lithium battery industry will officially enter the era of TWh.

Article source: high industrial lithium electricity